Deducting business meal costs: the 70% rule explained

In Germany, you deduct business meal (hospitality) costs with clients or partners at 70% of the reasonable amount as a business expense; the remaining 30% is non-deductible. Input VAT, by contrast, is recoverable at 100% if you hold a proper invoice. The condition is a complete hospitality receipt stating the purpose, participants, place, date, and amount.

Updated: June 2026

The 70/30 split in a worked example: 70% of the net amount is deductible as a business expense, while the VAT is 100% recoverable as input VAT.

Basis: § 4 (5) no. 2 EStG · § 15 (1a) UStG

What counts as a business meal cost?

Hospitality costs cover the food and drink provided to people: meals, beverages, and customary extras such as tips or cloakroom fees. What matters is that the meal has a business or operational purpose.

The classic case is a business meal at a restaurant: you invite a client, a supplier, or a prospect and discuss a specific project over lunch or dinner. Catering in a meeting room or a working meal while travelling can also qualify as hospitality.

Not every small courtesy is hospitality, though. Coffee, water, and biscuits during a meeting count as a customary gesture and do not fall under the deduction cap.

Business-partner meal or internal meal?

The occasion matters first. For a meal with an external business reason (clients, partners, or prospects), only 70% of the costs are deductible. This also applies when your own employees join the table alongside the external guests.

For a purely internal meal attended only by your own employees (for example an internal working lunch or a company event), the costs are generally 100% deductible. The 70% cap mainly concerns business meals with external partners.

For company events such as a summer party or Christmas dinner, German wage-tax law adds an allowance of EUR 110 per employee, for a maximum of two events per year. If the cost per employee stays below that allowance, no taxable wage arises, and the expense deduction for a purely employee event remains at 100%.

The 70% rule with a worked example

Of the reasonable net cost of a business-partner meal, 70% may be deducted as a business expense. The remaining 30% is not deductible. The legal basis is Section 4(5) sentence 1 no. 2 EStG.

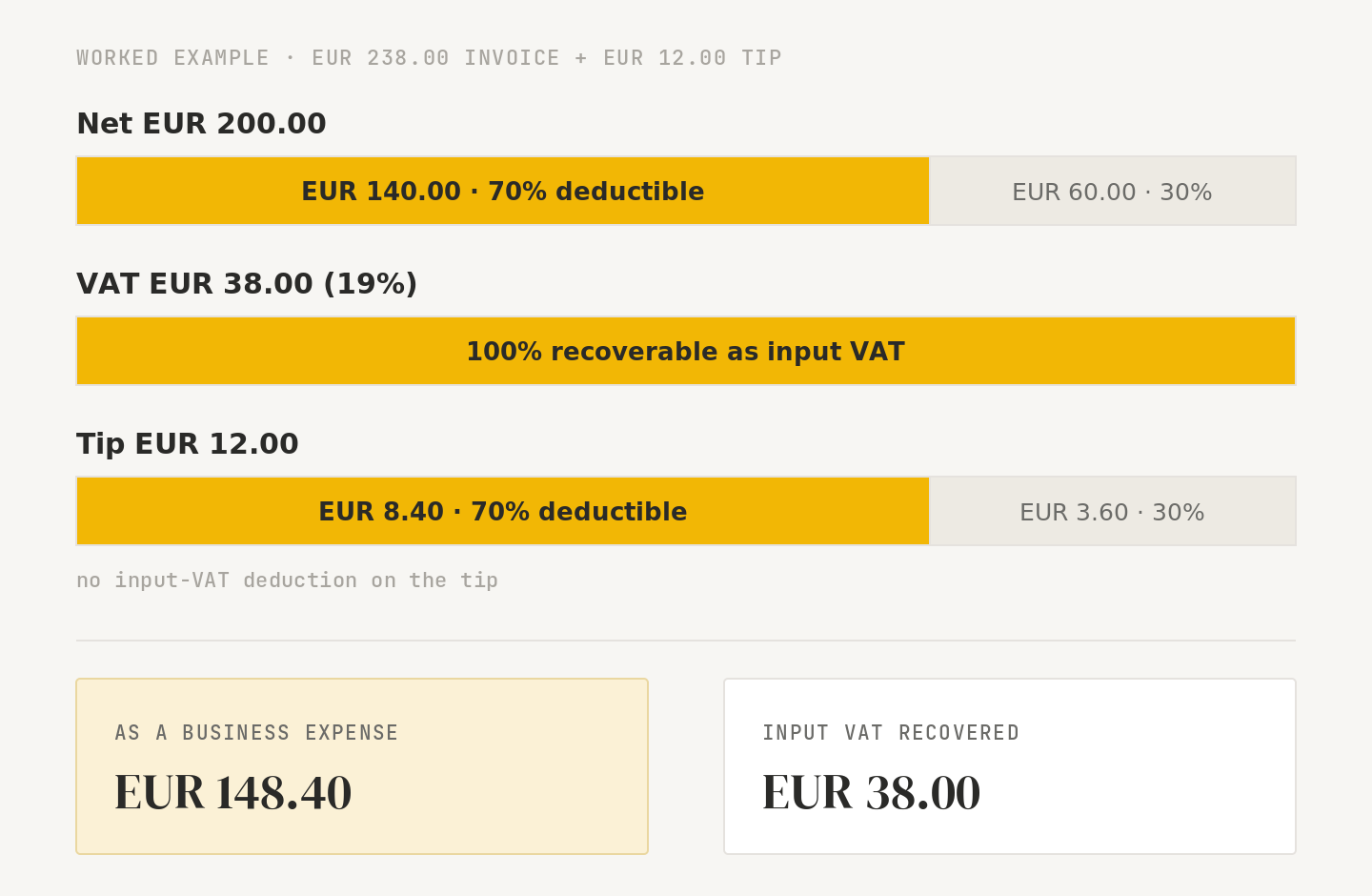

A worked example: after a business meal with two clients, you hold a restaurant invoice of EUR 238.00 gross, that is EUR 200.00 net plus EUR 38.00 VAT (19%). On top, you paid a tip of EUR 12.00 that does not appear on the invoice.

Item

Amount

Tax treatment

Restaurant invoice, gross

EUR 238.00

EUR 200.00 net + EUR 38.00 VAT (19%)

Input VAT

EUR 38.00

100% recoverable (with a proper invoice, Section 15(1a) UStG)

Business expense: 70% of EUR 200.00 net

EUR 140.00

deductible

30% of EUR 200.00 net

EUR 60.00

not deductible

Tip (no VAT shown), at 70%

EUR 8.40

deductible (of EUR 12.00)

In total, you deduct EUR 140.00 plus EUR 8.40 as a business expense and recover the full input VAT of EUR 38.00. Non-deductible are EUR 60.00 of the net invoice amount and EUR 3.60 of the tip.

In your bookkeeping, separate the two portions from the start: the standard German charts of accounts provide separate accounts for deductible and non-deductible hospitality expenses. That way the 70/30 split is cleanly documented for your profit calculation.

Input VAT: 100% recoverable

Unlike the expense deduction, input VAT is recoverable in full, at the whole 100% rather than 70%. Section 15(1a) UStG states this explicitly. The requirement is a proper invoice under Section 14 UStG showing the VAT separately.

That is exactly why the original restaurant invoice matters: you cannot reclaim VAT from a mere self-issued receipt (Eigenbeleg). There is also no VAT recovery on the tip, because no VAT is shown for it.

Reasonableness

Only reasonable expenses are deductible. What counts as reasonable depends on the industry, the occasion, the size of the business, and the importance of the relationship; there is no fixed euro limit.

An upscale business meal to close a contract with a key client can be reasonable; a luxury menu for a routine catch-up usually is not. Excessive amounts can be reduced proportionally, and only the reasonable part enters the 70% deduction.

The documentation duties: place, date, participants, purpose, amount

Section 4(5) sentence 1 no. 2 EStG requires written proof. The following details are mandatory:

place of the meal

date of the meal

participants: all guests by name, including the host

purpose of the meal, stated specifically rather than as a generic 'business lunch'

amount of the expense (including tip)

If the meal takes place at a restaurant, you must attach the invoice; the purpose and participants are then added on the invoice itself or on a separate record. Be precise about the purpose: 'project meeting on the website relaunch with Muster GmbH' is convincing, a bare 'client meeting' can trigger questions.

Complete the record promptly, while the participants and purpose of the business meal are still fresh. If individual details are missing or too vague, the tax office can deny the deduction for the entire meal.

Requirements for the restaurant invoice

If the venue uses an electronic till with a certified technical security device (TSE), the invoice must be machine-generated and electronically recorded, per the Federal Ministry of Finance (BMF) circular of 30 June 2021. It then includes, among other things, the TSE transaction and serial number and the start and end times of the transaction.

A purely handwritten restaurant receipt is therefore, as a rule, no longer sufficient within Germany. The self-issued receipt only adds the details missing from the machine invoice (purpose, participants) and the tip.

Two amount thresholds matter. Up to EUR 250 gross, a simplified small-amount invoice under Section 33 UStDV with reduced details is sufficient. Above EUR 250, the name of the host must additionally appear on the invoice; ideally, ask the restaurant to add it on the spot.

There is an exception for meals abroad: a handwritten invoice can exceptionally be accepted if you credibly show that the country in question has no requirement for machine-generated receipts. More on this in the guide to hospitality receipts abroad.

Hospitality or gift? Where the line runs

Not everything you give a business partner is hospitality. If you hand a client a bottle of wine to take home, that is a gift, and gifts follow their own tax rules, including the EUR 35 limit.

Hospitality presupposes that food and drink are consumed on the spot, typically at a shared business meal. For the 70% rule, what counts is consumption as part of the meal, not handing over goods.

Checklist for the expense deduction

machine-generated original invoice on hand

purpose specifically stated

all participants recorded by name

tip separately evidenced

for amounts over EUR 250, host name on the invoice

reasonableness checked

70% booked as a business expense, 30% as non-deductible

input VAT claimed at 100%

When the receipt is missing or lost

If the original is missing or incomplete, the deduction is not automatically lost. For this situation, a replacement hospitality receipt can be created; the guide hospitality receipt lost: what to do explains how.

How such a self-issued receipt fares with the German tax office, and what it depends on, is covered in Eigenbeleg for business meals at the tax office. Keep in mind: without a proper invoice, the input-VAT recovery is gone.

This article is not tax advice. Recognition is decided on a case-by-case basis by the relevant tax authority.

Frequently asked questions

Why are only 70% of business meal costs deductible?

The law assumes a partly private element in business meals. Under Section 4(5) no. 2 EStG only 70% of the reasonable net cost is deductible.

How does the 70/30 split work in practice?

You split the net amount of the invoice: 70% is booked as a deductible business expense, 30% as non-deductible. With EUR 200 net, that is EUR 140 deductible and EUR 60 non-deductible.

Can I recover the full input VAT even though only 70% is deductible as an expense?

Yes. Under Section 15(1a) UStG, input VAT is 100% recoverable, provided a proper invoice exists. The 70% cap only concerns the expense deduction.

Create a replacement business meal receipt by chat.

Send a photo in chat. The details are captured. You receive your replacement hospitality receipt as a PDF.

Get started

Opens Telegram · No registration required