Self-issued receipts for business meals: what the German tax office accepts

For business meal expenses, a self-issued receipt (Eigenbeleg) is only an emergency fallback, not an equivalent substitute for the restaurant bill. Formally, the German tax authorities require a machine-generated, electronically recorded invoice for restaurant hospitality. Whether the tax office nevertheless accepts a self-created document is a case-by-case decision. Good supporting evidence improves the odds, but there is no guarantee.

Updated: June 2026

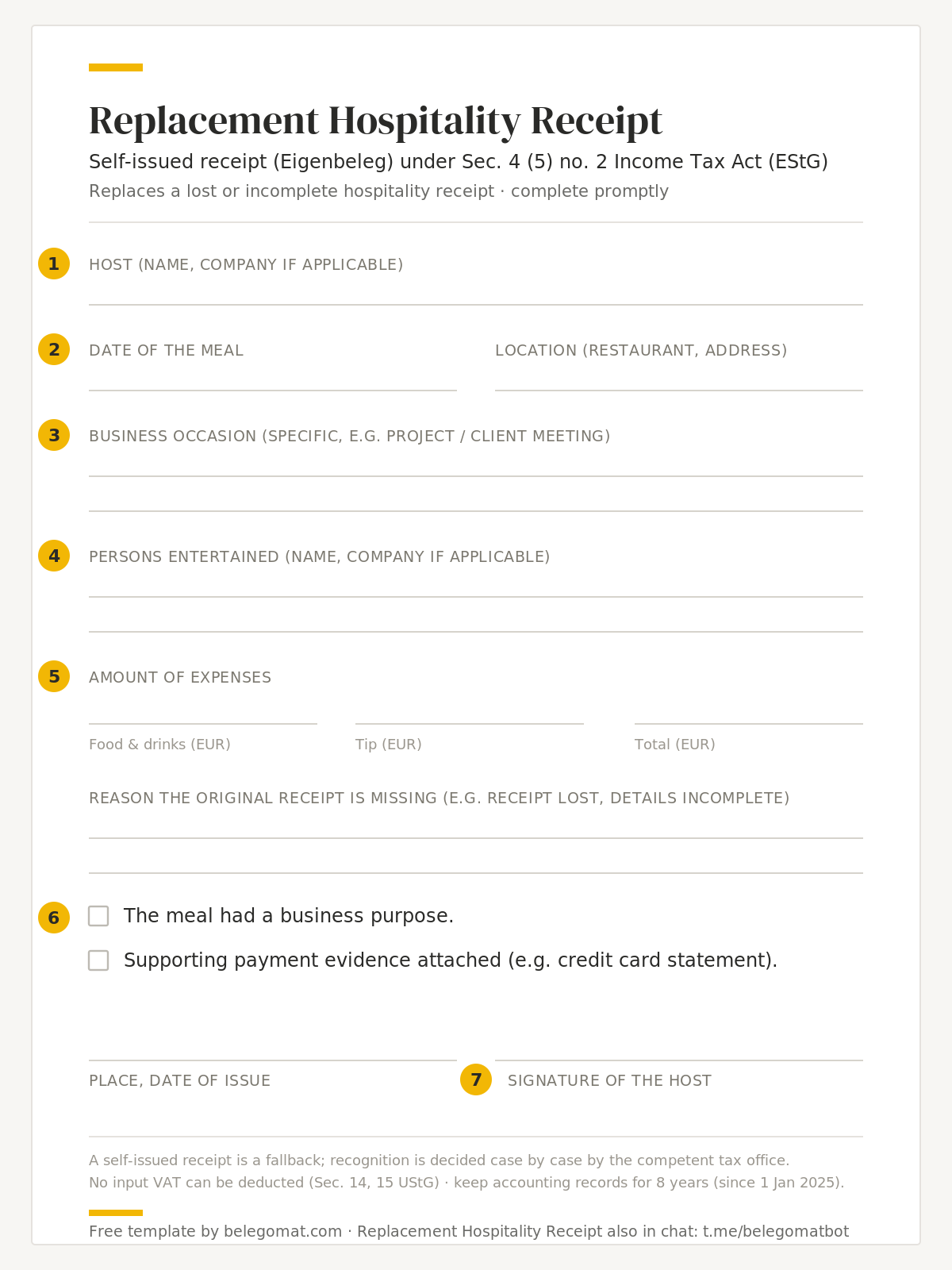

Annotated sample replacement hospitality receipt showing the seven required fields under § 4 (5) no. 2 EStG.

The short answer

For most missing receipts, a self-issued receipt is an established remedy: you document the expense yourself, make it credible, and the deduction is usually secured. For business meal costs, the rules are stricter. The law and the administrative guidance explicitly tie the deduction of restaurant hospitality to the restaurant's own invoice: specifically, a machine-generated, electronically recorded one.

A self-issued receipt does not meet this formal requirement. It can save the deduction if the original is missing through no fault of your own and you can demonstrate the expense convincingly, for example with a credit card statement. But there is no legal entitlement to recognition: the tax office decides case by case, and it may refuse the deduction in whole or in part.

There is a reason for the strictness: hospitality expenses sit close to private living costs, which is why the legislator attached special documentation duties to them. A lost parking ticket arouses no suspicion of abuse, but from the administration's perspective a restaurant visit looks more questionable. This assessment runs through every rule on the subject.

Two things are certain from the outset: input VAT is always lost with a self-issued receipt, and the higher the amount, the more critically the authorities will look. Knowing this lets you plan realistically and make the best of a bad situation when it happens.

The legal framework at a glance

The requirements for hospitality receipts come from three levels that build on each other:

Section 4(5) sentence 1 no. 2 EStG is the statute. It limits the deduction of business hospitality costs to 70 percent of the reasonable expenses and requires written details of place, date, participants, occasion, and amount. For meals in a restaurant, the invoice must be attached.

R 4.10 EStR are the income tax guidelines. They are administrative instructions binding on the tax offices and spell out how the statutory requirements are checked in practice.

The BMF circular of 30 June 2021 (IV C 6 – S 2145/19/10003 :003) is the currently authoritative set of detailed rules. Among other things, it stipulates that the restaurant invoice must be machine-generated and electronically recorded, and it covers digital hospitality records and meals abroad.

The hierarchy matters: the statute sets the frame, while guidelines and BMF circulars bind the tax administration but not the tax courts. In practice, though, your tax office will check exactly against these administrative rules. Submitting a self-issued receipt means deliberately stepping outside the intended standard path.

Why the machine-generated invoice matters so much

Since the German Cash Register Security Ordinance (KassenSichV), electronic point-of-sale systems in Germany must be equipped with a certified technical security device (TSE). Every till receipt is recorded in a tamper-proof way. This is exactly what the tax authorities rely on: the hospitality invoice should come from such a system, because it then cannot be manipulated after the fact.

You can recognise a receipt from such a till system by its machine-printed details, for example a transaction number, the till or serial number, and the exact start and end time of the transaction. These are precisely the features auditors look at when judging whether a hospitality receipt is genuine.

This leads to a consequence that surprises many: handwritten bills or informal receipts are not sufficient within Germany, even if their content is complete. A "bill" filled out by hand by the waiter is not a proper hospitality receipt for tax purposes.

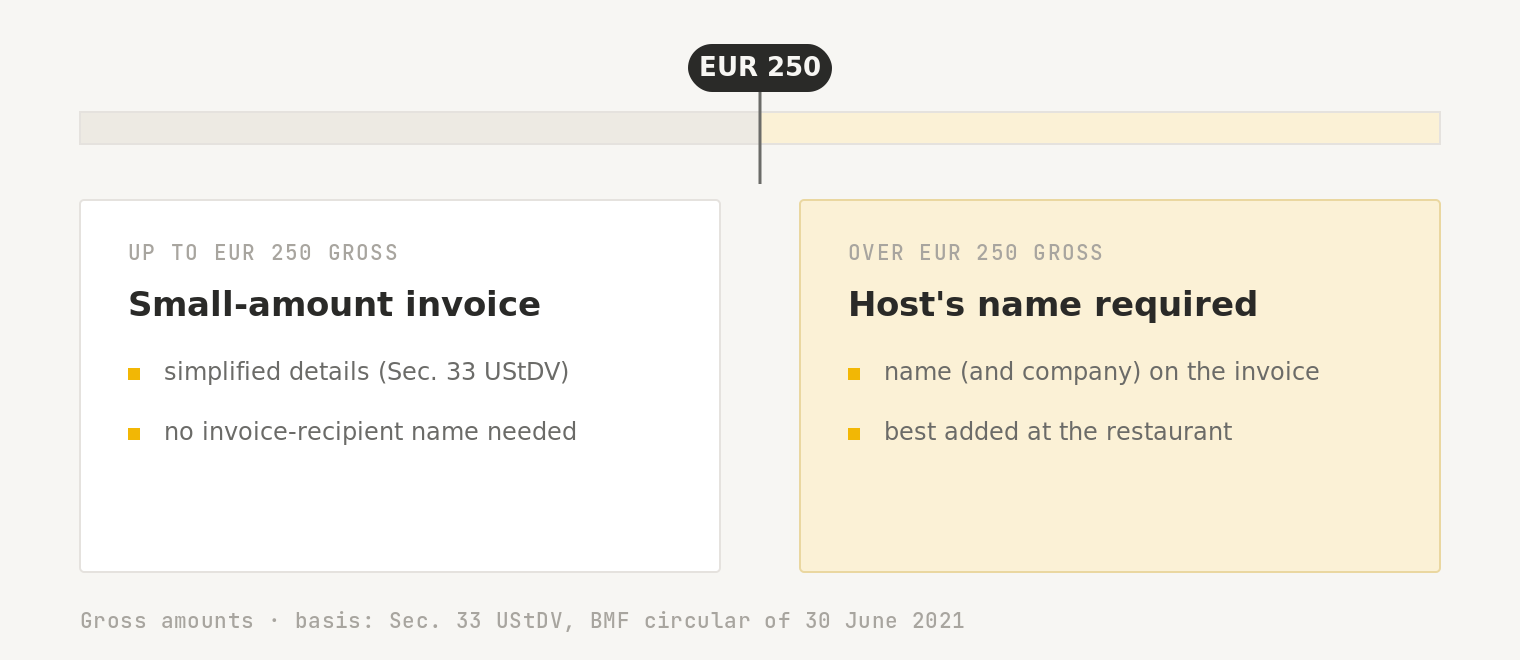

An amount threshold also applies: for invoices over 250 euros, the name of the host (yours or your company's) must appear on the invoice. It is best to have the name added directly at the restaurant, as this is hard to fix afterwards. Up to 250 euros, a small-amount invoice under Section 33 UStDV without recipient details is sufficient.

The EUR 250 threshold: up to EUR 250 gross a small-amount invoice suffices; above it, the host's name must appear on the invoice.

Basis: Sec. 33 UStDV · BMF circular of 30 June 2021

If you have a formally correct invoice, all that remains is adding the hospitality details. The guide on deducting business meal costs shows how.

When a self-issued receipt still has a chance

The fact that the self-issued receipt is not the intended route does not make it hopeless. In practice, it comes into play in three situations:

1. The receipt was lost. If the meal undisputedly took place and you can prove the payment via the credit card statement or bank statement, a promptly created self-issued receipt can document the transaction. The proof of payment is your strongest argument: it evidences date, place, and amount from an independent source. The article on what to do when a hospitality receipt is lost covers the details.

2. The invoice exists but is incomplete. If only the hospitality details are missing (occasion, participants, signature), you do not need a full self-issued receipt. You may add these details on a supplementary document attached to the original invoice. This is the much safer route, because the machine-generated invoice is preserved.

3. The meal took place abroad. There, too, the machine-generated receipt is the standard. However, a handwritten invoice can exceptionally suffice if you credibly demonstrate that the country in question has no obligation to issue machine-generated receipts. More on this in the article on hospitality receipts from abroad.

In all cases, credibility is decisive: prompt creation, complete details, and a plausible amount. Prompt means ideally the same day or within the following days, since a reconstruction from memory months later convinces no one. The tax office may estimate the expense under Section 162 AO, meaning it can also reduce the deduction if the self-issued receipt does not fully convince. A realistic amount backed by proof of payment is worth more than a generously rounded one.

One point that is often underestimated: frequency matters. A single, well-documented self-issued receipt per year is a credible exception. Anyone who routinely accounts for business meals with self-issued receipts signals an organisational problem to the tax office, and risks the rest of their records being examined more critically too.

The input VAT trap

The most expensive side effect of a lost hospitality receipt concerns VAT: no input VAT can be recovered from a self-issued receipt. Sections 14 and 15 UStG require a proper invoice with VAT shown separately, and a self-created document cannot replace that, no matter how carefully it is prepared.

This stings because the VAT treatment of business meals is otherwise generous: with a proper hospitality invoice, input VAT is 100 percent deductible, even though the income tax deduction is capped at 70 percent. This special rule is found in Section 15(1a) UStG. The 30 percent disallowance for profit purposes does not carry over to VAT.

With a self-issued receipt you lose exactly this advantage: the entire VAT contained in the bill is permanently gone, and only 70 percent of the gross amount is deductible as a business expense. A simple example: on a bill of €119 (including 19 percent VAT), a proper receipt lets you deduct the full €19 of input VAT plus €70 as a business expense. With a self-issued receipt, the input VAT is gone entirely, and only 70 percent of the gross amount remains deductible.

That is the sober reason why trying to obtain a duplicate from the restaurant is almost always worth it before reaching for a self-issued receipt. For small amounts the loss may be bearable; for a client dinner running to several hundred euros, it is not.

Thresholds and deadlines at a glance

Rule

Value

Basis

Deduction limit for business hospitality

70% deductible, 30% not

Section 4(5) no. 2 EStG

Input VAT deduction with a proper invoice

100%

Section 15(1a) UStG

Small-amount invoice (simplified details)

up to €250 gross

Section 33 UStDV

Host's name must appear on the invoice

above €250

BMF circular of 30 June 2021

Allowance for company events

€110 per employee, max. 2 events/year

Section 19(1) sentence 1 no. 1a EStG

Retention period for accounting records

8 years (since 1 Jan 2025, previously 10)

Section 147 AO, Fourth Bureaucracy Relief Act

Meals for employees on internal business occasions

100% deductible

no reduction under Section 4(5) no. 2 EStG

The last row is often overlooked: the 70 percent cap only applies to business hospitality, meaning meals with business partners, clients, or other external guests. A purely internal meal for your own employees, for example during an in-house meeting, is fully deductible.

Practical recommendation: the right order

If the hospitality invoice is missing or defective, work through the options in this order:

Ask for a duplicate. Modern POS systems store every transaction. Many restaurants can reprint a receipt or send it as a PDF; with the date and time, staff can usually find the booking quickly. This is the only solution that also rescues the input VAT deduction.

Secure proof of payment. Download the credit card statement or bank statement and file it with the transaction. It will later be the backbone of your credibility.

Create a replacement receipt with all mandatory details. Only if no duplicate can be obtained should you promptly create a replacement hospitality receipt.

For the replacement receipt to stand a realistic chance, it must be complete. The seven mandatory details:

occasion of the meal, stated specifically rather than just "business dinner"

host

person(s) entertained

place and date

amount including the tip

statement of the business purpose

signature

Record the details as specifically as possible: not "business dinner with client", but rather "meeting on warehouse logistics project proposal with Ms Muster, Beispiel GmbH". The more precise the occasion, the less surface the receipt offers for attack. Then file it like any accounting record, organised and tamper-proof, so it can be produced immediately during an audit.

Belegomat is a chat service that turns a photo of a restaurant receipt into a structured German-compliant replacement hospitality receipt (Eigenbeleg) as a PDF. How it works in detail is shown on the page create a replacement hospitality receipt by chat.

Conclusion

For business meals, the self-issued receipt is the last line of defence, not a convenient plan B. The German tax authorities formally require a machine-generated restaurant invoice; a self-created document is recognised only case by case, and most likely with proof of payment, prompt creation, and all seven mandatory details. It never rescues the input VAT. If you follow the order of duplicate, proof of payment, replacement receipt, you will get the best possible outcome from a bad situation.

This article is not tax advice. Recognition is decided on a case-by-case basis by the relevant tax authority.

Frequently asked questions

Does the German tax office accept a self-issued receipt instead of the restaurant bill?

Not as a matter of course. Formally, the tax authorities require a machine-generated restaurant invoice. A self-issued receipt is a fallback, and the tax office decides on its recognition case by case; proof of payment and complete details improve the odds.

Does the 250-euro threshold also apply to hospitality receipts?

Yes, in two ways: up to 250 euros, a small-amount invoice under Section 33 UStDV without recipient details is sufficient. Above 250 euros, the name of the host must additionally appear on the invoice.

What happens during a tax audit?

Hospitality receipts are typically examined closely. If the formal requirements are not met, the deduction can be denied or the amount estimated under Section 162 AO. Frequent self-issued receipts raise additional doubts about the bookkeeping.

Create a replacement business meal receipt by chat.

Send a photo in chat. The details are captured. You receive your replacement hospitality receipt as a PDF.

Get started

Opens Telegram · No registration required