You create a self-issued receipt (Eigenbeleg) by writing down the payee, the type of expense, the date, the amount and the business reason, then dating and signing the document. This is allowed whenever an original receipt is missing, unreadable, or was never issued. This guide explains step by step what a correct self-issued receipt looks like, what applies for input VAT, and where the limits are.

Updated: June 2026

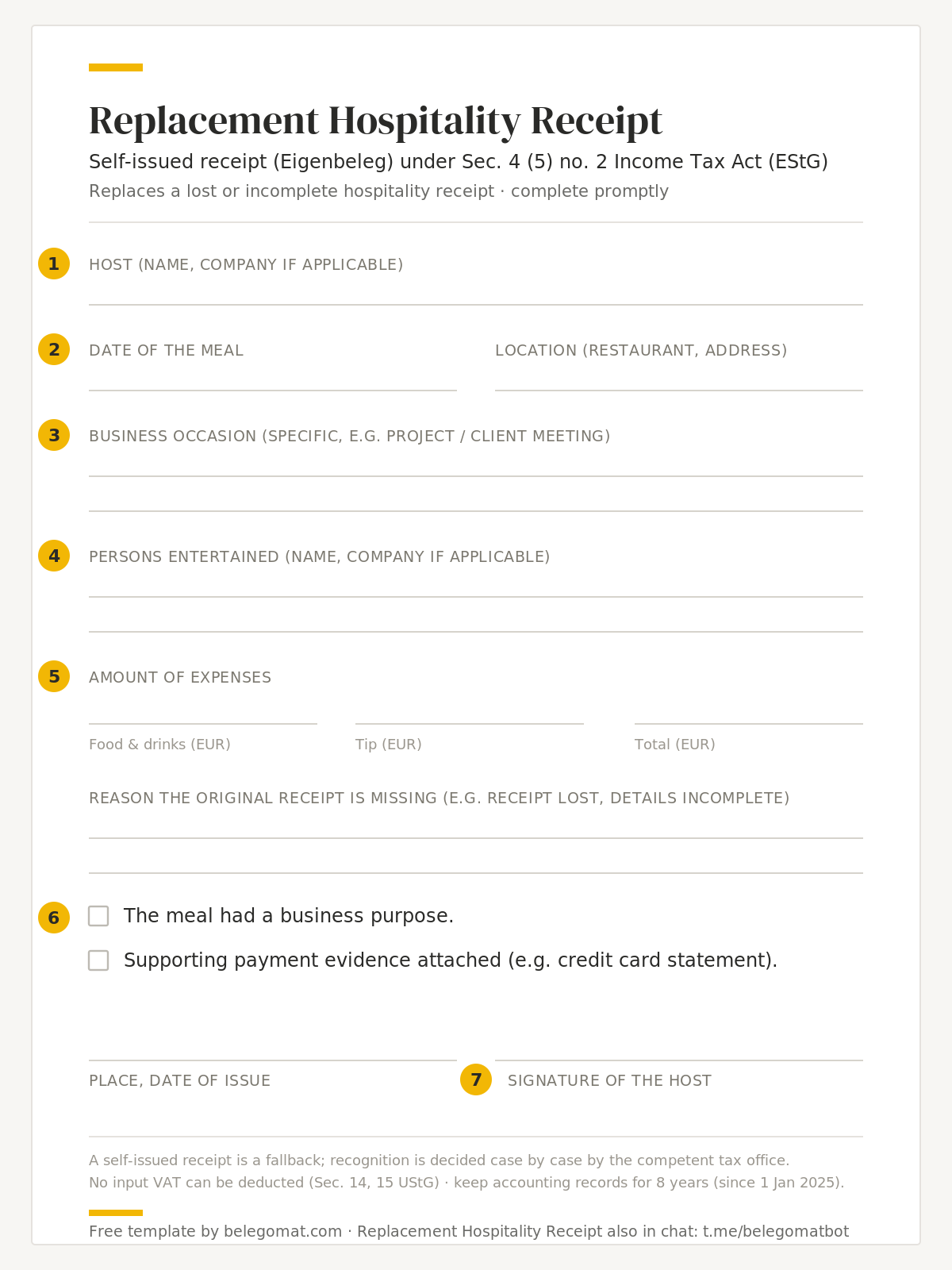

Annotated sample replacement hospitality receipt showing the seven required fields under § 4 (5) no. 2 EStG.

What is a self-issued receipt?

A self-issued receipt (Eigenbeleg) is a document you create yourself to replace a missing original. German bookkeeping follows the principle of no entry without a receipt: every business expense must be evidenced by a document. If, as an exception, no third-party receipt can be obtained for a business expense, you may issue the receipt yourself.

An Eigenbeleg is therefore not a blank cheque but a documented exception. Its purpose is to make an expense that actually occurred credible and verifiable, so the deduction does not fail just because a slip of paper was lost.

The distinction from a third-party document matters: a receipt issued by your business partner naturally carries more evidential weight. A self-issued receipt comes from you, which is exactly why the tax office (Finanzamt) expects it to be complete and plausible.

When is a self-issued receipt allowed?

An Eigenbeleg may only be used when no original receipt exists, because it was lost, is illegible, or was never issued. Typical cases:

a tip that does not appear on the bill

vending machines without a receipt (parking, stamps, coin machines)

lost or faded thermal-paper receipts that can no longer be read

small cash purchases for which no receipt was issued

business meals abroad where the receipt lacks details required in Germany

A business purpose is always required. Private expenses cannot be brought into the books via a self-issued receipt.

Anything that additionally supports the expense helps: a bank statement, a credit-card statement, a photo of the parking machine, or a calendar entry for the meeting. Supporting evidence like this makes a self-issued receipt considerably more credible.

When a self-issued receipt is not enough

The Eigenbeleg stays the exception. Routinely replacing originals with self-issued receipts invites questions during a tax audit, and frequent self-issued receipts weaken the credibility of the whole bookkeeping.

If an original exists, it must be used. If the original can still be obtained (for example a copy of the invoice from the restaurant or retailer), that route takes priority too. And for input-VAT recovery a self-issued receipt is not sufficient anyway (more on this below).

The size of the expense also plays a role: a self-issued receipt for a small parking fee rarely raises questions. The higher and more unusual the amount, the more important supporting evidence such as a credit-card statement becomes.

What must a self-issued receipt contain?

For the tax office to accept a self-issued receipt, it should include:

name and address of the payee

type of expense: what was bought or paid for?

date of the expense

amount, itemised and as a total where applicable

reason / business purpose

date of issue and a signature

For a business meal, the special details under Section 4(5) no. 2 EStG also apply: purpose, host, guests, and place and date. This case is called a replacement hospitality receipt, a special form of the Eigenbeleg with stricter requirements.

Step by step: how to create a self-issued receipt

Whether on paper, as a PDF, or with a generator, the process is always the same. Six steps are enough:

Confirm that no original receipt can (still) be obtained.

Note the payee, type, date, and amount of the expense promptly.

Briefly justify the business purpose.

For a business meal, add purpose, host, and participants.

Date the receipt and sign it.

Attach supporting evidence where available (e.g. bank or credit-card statement).

Tip: the sooner you document, the more credible the receipt. Reconstructing from memory weeks later is far less convincing to the tax office.

Example: what a finished self-issued receipt looks like

The list of mandatory details may sound abstract, but in practice a self-issued receipt is written in minutes. A typical case: the parking machine at a client meeting does not print a ticket. The receipt could look like this:

Self-issued receipt (Eigenbeleg)

Payee: Parkhaus am Stadttor GmbH, Musterstrasse 12, 50667 Cologne

Type of expense: parking fee (parking machine)

Date of expense: 14 May 2026

Amount: EUR 8.50

Reason no receipt exists: the parking machine did not issue a ticket.

Business purpose: client meeting at Beispiel GmbH, Cologne (project review).

Issued on: 14 May 2026

Signature: Max Mustermann

That is all it takes: payee, type, date, amount, reason, and a signature. If you also keep the calendar entry for the client meeting, you already have a second piece of evidence for a later audit.

Template or generator?

You do not have to draft a self-issued receipt from scratch every time. A ready-made template you can download makes sure no mandatory field is forgotten: fill it in, sign it, file it.

A generator that asks for the details and produces a finished PDF is faster still. Which solution makes sense when is covered in our comparison of Eigenbeleg generators.

Self-issued receipts and VAT: the key limitation

As a rule, you cannot reclaim input VAT from a self-issued receipt. Input VAT recovery requires a proper invoice under Section 14 UStG that shows the VAT separately.

So the Eigenbeleg secures the deduction of the (net) expense, but not the input VAT. To reclaim VAT you need the original invoice.

In practice this means that with a lost restaurant bill of EUR 119, a self-issued receipt rescues the cost as a business expense, but the EUR 19 of VAT is lost as input VAT. That alone is a good reason to ask the issuer for a copy of the invoice first.

Self-issued receipts and GoBD: digital is allowed

A self-issued receipt may be created on paper or digitally. What matters is compliance with the GoBD principles for proper bookkeeping: comprehensible, complete, and tamper-evident. A photo or scan is acceptable as long as it is stored in an audit-proof way and later changes remain visible.

Concretely: the receipt must be created promptly, be clearly attributable to a booking, and be protected against silent overwriting. A PDF in your accounting system or a properly filed scan usually meets this standard; a loose text file that can be changed at any time without trace usually does not.

A digitally created Eigenbeleg still needs all the mandatory content and should be signed: on paper, or as a scanned or otherwise traceably documented confirmation by the issuer.

Retention: eight years for accounting documents

Like all accounting documents, the self-issued receipt is subject to statutory retention periods. Since 1 January 2025, accounting documents must be kept for eight years; previously it was ten. The period was shortened by the Fourth Bureaucracy Relief Act.

Receipts must be stored in an orderly way so they can be presented during an audit. Digitally filed self-issued receipts must remain readable and unchanged for the entire retention period.

Common mistakes

Most self-issued receipts fail not because of the principle but because of avoidable gaps. These are the points auditors typically notice first:

The reason for the expense is missing or too general.

The amount is not clearly stated.

The signature is missing.

A self-issued receipt is created even though the original still exists.

For a business meal, the additional details under Section 4(5) no. 2 EStG are missing.

Conclusion

A self-issued receipt is an accepted tool when an original is missing, provided it is complete, plausible, and business-related. You cannot reclaim input VAT from it, and business meals carry additional mandatory details.

If you know the required fields, document promptly, and attach supporting evidence, your chances of acceptance are good. There is no guarantee, though, because the Finanzamt decides each case individually. And do not forget the eight-year retention period.

This article is not tax advice. Recognition is always decided case by case by the competent tax office (Finanzamt).

Frequently asked questions

How many self-issued receipts may I create?

There is no fixed limit, but they should remain the exception. Frequent self-issued receipts can trigger questions during an audit.

Does a self-issued receipt need a signature?

A signature is strongly recommended, as it confirms the details and increases credibility.

Is a bank statement enough to replace the receipt?

A bank statement only proves the payment, not the reason for the expense. It is good supporting evidence alongside a self-issued receipt, but it does not replace one.

Create a replacement business meal receipt by chat.

Send a photo in chat. The details are captured. You receive your replacement hospitality receipt as a PDF.

Get started

Opens Telegram · No registration required